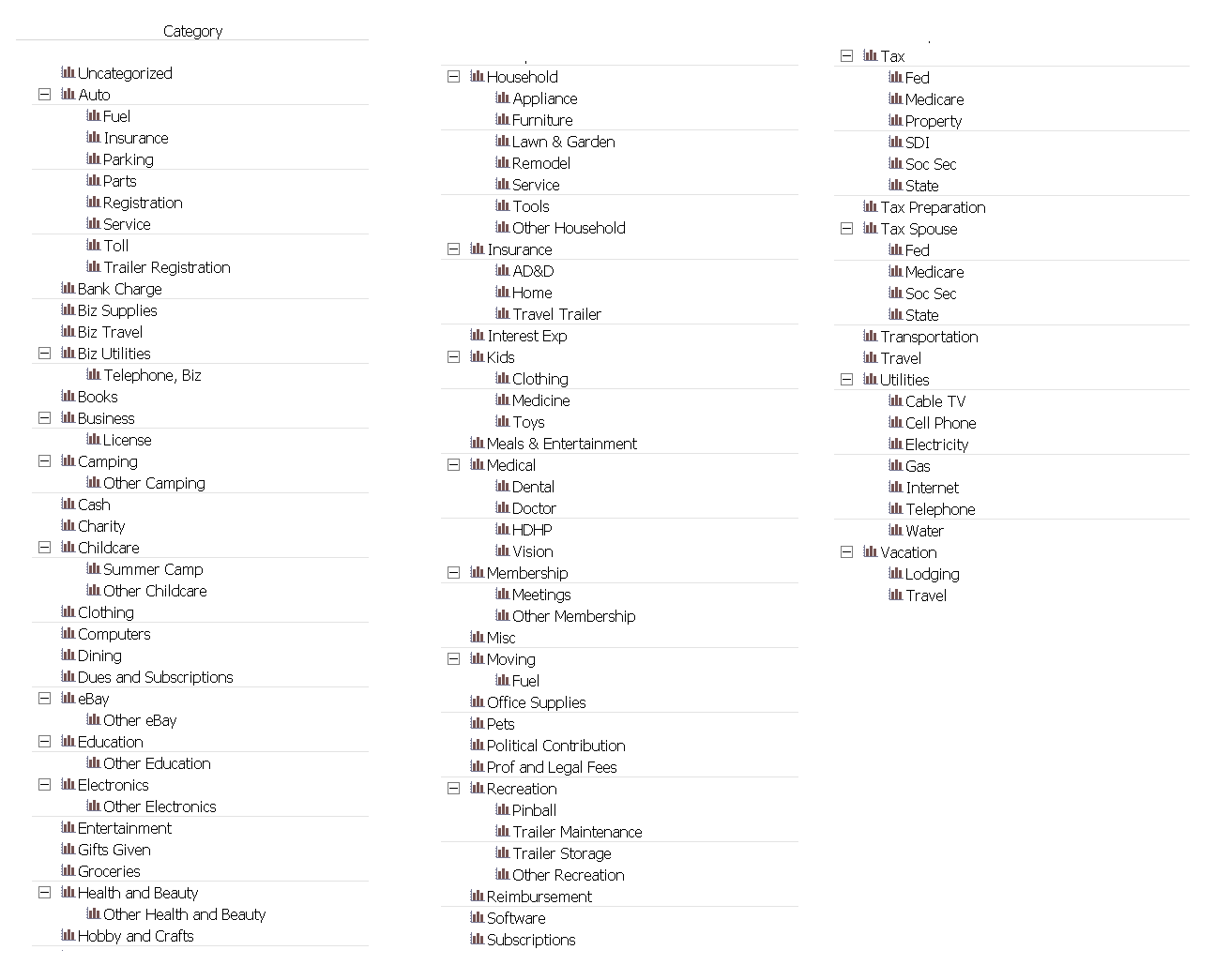

Right now I have the below 10 Groups and 69 Categories and feel like I could potentially do a better job consolidating. I’ve listed them the below for reference.

For those who feel like they aren’t over-granularizing their expense tracking, would you care to critique mine or better yet share your Groups/Categories?

Note: I own a home, car, pet, no kids

| Category | Group |

|---|---|

| Mortgage | Home |

| Yard | Home |

| Garbage | Home |

| Cleaning Service | Home |

| Home Improvement | Home |

| Home Maintenance | Home |

| Home Furnishings | Home |

| Home General | Home |

| Water | Utilities |

| Alarm | Utilities |

| Electricity | Utilities |

| Gas | Utilities |

| Cable | Utilities |

| Internet | Utilities |

| Cell Phone | Telecom |

| Auto + Home Insurance | Insurance |

| Subscriptions | Telecom |

| Car Gas | Auto |

| Car Service + Maintenance | Auto |

| Rideshare | Auto |

| Parking | Auto |

| Car Wash | Auto |

| Tickets | Auto |

| Registration + License | Auto |

| Groceries | Food + Drink |

| Restaurants + Alcohol | Food + Drink |

| Coffee + Tea | Food + Drink |

| Food Misc. | Food + Drink |

| Gym | Health |

| Doctor | Health |

| Dentist | Health |

| Medication | Health |

| Vet | Pets |

| Grooming | Pets |

| Dog Food | Pets |

| Dog Supplies | Pets |

| Boarding + Walking | Pets |

| Pet Insurance | Pets |

| Dog Training | Pets |

| Personal Care | Personal |

| CVS Misc. | Personal |

| Hair + Nails | Personal |

| Massage | Personal |

| Beauty | Personal |

| Dry Cleaners | Personal |

| Tailor + Alterations | Personal |

| Travel | Discretionary |

| Shopping | Discretionary |

| Gifts - Friends | Discretionary |

| Gifts - Family | Discretionary |

| Gifts - Us | Discretionary |

| Amazon Misc. | Discretionary |

| Entertainment | Discretionary |

| Club Memberships | Discretionary |

| Books | Discretionary |

| Education | Discretionary |

| Discretionary | |

| Hobbies | Discretionary |

| Business Services | Discretionary |

| Amex Membership | Discretionary |

| Gaming | Discretionary |

| Discretionary Misc. | Discretionary |

| Dept. of Revenue Tax | Taxes |

| US Treasury Tax | Taxes |

| Income Tax | Taxes |

| Property Tax | Taxes |

| Car Restoration | Outlier |

| Car Purchase | Outlier |

| Charity | Donations |